Should I Refinance for a Lower Rate? A Simple Rule of Thumb That Actually Works

Is Refinancing Your Mortgage Worth It? A Complete Guide to Making the Right Decision

Is refinancing worth it? Refinancing your mortgage used to be straightforward. When interest rates dropped, homeowners would call their lender and secure a lower monthly payment. Today’s landscape is more complex, with fluctuating mortgage rates, higher closing costs, and conflicting market information making the decision less clear-cut.

If you’re wondering whether refinancing is worth it or if you’d be throwing money away, you’re not alone. This guide will walk you through a reliable method to determine if refinancing makes financial sense for your situation.

Why Homeowners Refinance Their Mortgages

Mortgage refinancing can be an excellent financial strategy when executed properly. However, the benefits must clearly exceed the costs. Common reasons homeowners choose to refinance include:

- Reducing their monthly mortgage payment

- Shortening their loan term to build equity faster

- Consolidating high-interest debt into their mortgage

- Removing private mortgage insurance (PMI)

- Accessing home equity for major expenses

- Converting from an adjustable-rate mortgage (ARM) to a fixed-rate loan

The challenge lies in the upfront expense. Refinancing closing costs typically range from 2 to 3 percent of your loan amount. Without careful analysis, what seems like a smart move can become an expensive mistake.

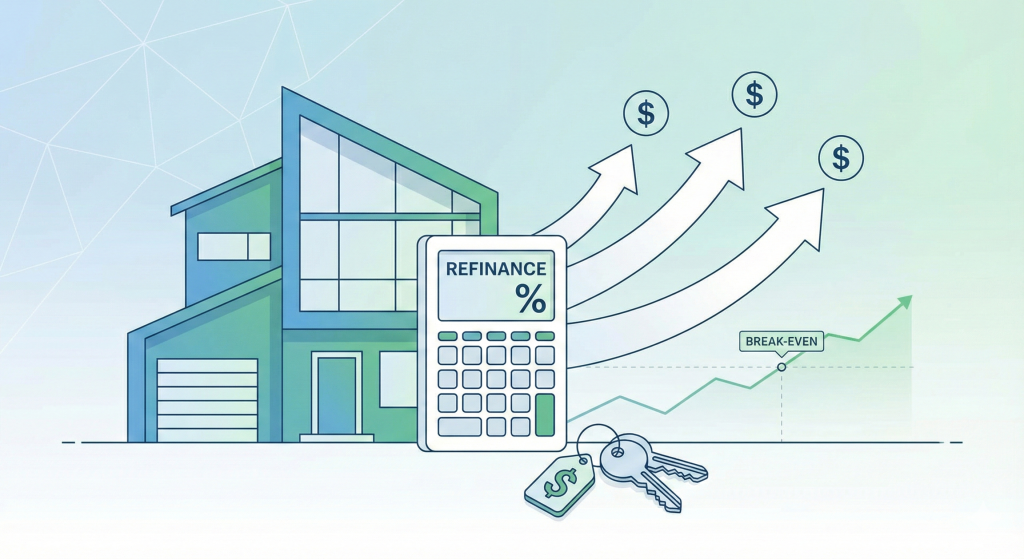

So, Is Refinancing Worth It? Here’s How to find your break-even point

The mortgage industry’s most valuable and underutilized tool is the break-even point calculation. This simple metric tells you exactly how long it will take for your monthly savings to recover your refinancing costs.

The general guideline is this: if you can recover your closing costs through monthly savings within 24 to 36 months, refinancing typically makes financial sense.

How to Calculate Your Break-Even Point

The formula is straightforward:

Total Closing Costs divided by Monthly Payment Savings equals Months to Break Even

Here’s a practical example:

- Closing costs: $6,500

- Monthly savings: $200

- Break-even period: 32.5 months

If you plan to remain in your home for at least 33 months, this refinance would be worth considering. If you’re thinking about selling or moving sooner, refinancing probably isn’t your best option.

Most lenders won’t calculate this for you automatically, so it’s essential to run these numbers yourself or request a detailed analysis.

When Is Refinancing Worth It?

Reducing Your Interest Rate by 0.75% or More

Industry experience shows that lowering your rate by at least three-quarters of a percentage point typically generates enough savings to justify refinancing costs. This is especially true for loan amounts above $300,000, where even small rate reductions translate to significant monthly savings.

Eliminating Private Mortgage Insurance

If your home’s value has appreciated significantly since your original purchase, refinancing could remove PMI from your monthly payment. This alone can save several hundred dollars each month, making it one of the fastest paths to positive return on refinancing costs. Generally speaking, removing PMI makes refinancing worth it.

Switching to a Shorter Loan Term

Refinancing from a 30-year mortgage to a 20-year or 15-year term can save tens of thousands of dollars in lifetime interest payments. While your monthly payment may increase slightly, the long-term savings and faster equity building often make this strategy worthwhile, especially for homeowners approaching retirement.

Consolidating High-Interest Debt

If you’re carrying credit card balances with interest rates above 25 percent, consolidating this debt into your mortgage can dramatically improve your monthly cash flow. This strategy requires financial discipline to avoid accumulating new high-interest debt, but when used responsibly, it can be transformative for your overall financial health.

When Refinancing Isn’t Worth the Cost

Minimal Monthly Savings

If refinancing would only save you $50 per month, the math rarely works in your favor. Small savings take too long to recover thousands of dollars in closing costs.

Short Homeownership Timeline

Planning to sell within the next year or two? Refinancing typically doesn’t make sense unless you’re specifically targeting PMI removal or eliminating high-interest debt. The break-even period is simply too long for short-term homeowners.

Chasing Rates Without Strategy

A low interest rate isn’t the ultimate goal. Your focus should be on creating a comprehensive financial plan that aligns with your long-term objectives. Rate-shopping without considering your broader financial picture can lead to poor decisions.

Should You Refinance If You Already Have a Low-Rate Mortgage?

This is one of today’s most common refinancing questions. If you secured a mortgage when rates were at historic lows around 3 percent, conventional wisdom suggests you should keep that loan untouched.

However, there are legitimate scenarios where refinancing a low-rate mortgage makes sense:

- You need to access home equity for a major renovation or investment opportunity

- Removing PMI would provide substantial monthly savings

- You’re transitioning to a shorter loan term as part of retirement planning

- Improving your debt-to-income ratio to qualify for future financing needs

While low interest rates are valuable, your complete financial picture matters more than any single number. Sometimes the right move involves looking beyond just the interest rate.

Getting a Personalized Refinance Analysis

Every homeowner’s financial situation is unique. Cookie-cutter advice and general rules of thumb can only take you so far when making a decision that impacts hundreds of thousands of dollars.

A comprehensive refinance analysis should include:

- Your specific break-even point based on actual costs

- Estimated new monthly payment with different loan options

- Total interest savings over the life of the loan

- PMI removal potential and timeline

- Available home equity and how to access it strategically

- Debt consolidation scenarios with projected savings

- Side-by-side comparison of 30-year, 20-year, and 15-year terms

This level of detail removes the guesswork and gives you confidence in your decision.

Take the Next Step: Request Your Free Refinance Analysis

If you’re serious about understanding whether refinancing makes sense for your specific situation, a detailed financial analysis will provide the clarity you need.

A personalized refinance savings analysis will show you the real numbers, your actual options, and whether refinancing truly benefits your financial goals.

Get your free refinance analysis today with no obligation. I’ll walk you through the math, explain your options clearly, and help you make an informed decision about your mortgage.